Awash in Cash

If you had to guess at how quickly the US car wash industry was growing its revenues, what do you think it would it be?

A hint to help you out - the US car parc (i.e. total population of cars in the US) grew 10% over the past decade - less than 1% per year.

Source: Jeff Greenberg / Universal Images Group Editorial, via Bloomberg

Yet, somehow, the car wash industry - an industry one would expect should be fairly mature and stagnant given how long cars and car washes have been around - grew revenues 7%(!!) per year, annualized, over the past decade. Revenues grew from $7 billion in 2012 to $16 billion in 2022 - and look to continue growing.

I chanced on this remarkable statistic as I read this Bloomberg article about the sudden and rapid proliferation of car washes in the US. As I dug in further, the scale of the growth has further perplexed me, with increasing numbers of individuals concerned about the impact of too many car washes. But how does a sleepy industry suddenly see outsized growth?

I think that ultimately growth can be boiled down to simple equation, with two ( codependent) variables:

At the heart of the rebirth of the car wash industry are multiple trends that provide the opportunity part of the equation.

Do-It-For-Me (DIFM) - A simple concept that will pervade many consumer-focused industries moving forward, car washes are the quintessential business model benefiting from the DIFM trend. As our lives get more optimized, there's an growing trend of outsourcing many of the more menial and mundane elements of our lives that we previously preferred to do ourselves. This has led to increasing demand for businesses - also known as do-it-for-me (DIFM) businesses - that we gladly pay to buy back the time (or effort) that we would otherwise have to exert to learn how to and/or spend the time doing the mundane tasks. Additionally, there's been more complexities built into many of these activities - such as overly complicated electronics and regulatory costs - that make doing many of these tasks hard for the individual. Fewer and fewer of us know how to cook, how to fix our appliances, change our oil and tires - and DIFM businesses who specialize in these activities become the preferred provider to us.

With car washes, a combination of 1) consumers being less interested in washing their own cars at home, and 2) environmental regulations concerning excess water use and chemical use making it harder for consumers who want to wash their own cars at home, have led to an increased demand from car owners to pay car washes to take over the time, effort, and regulatory burden of car washing. As Millennials and Gen Zers, individuals who are less likely to have grown up with parents who washed and cleaned their own cars, age and become a larger part of the car owner population, and as regulatory regimes governing water and chemical use gets more complex, car wash demand will only continue to grow.

A New (Subscription) Model - Car washes have also discovered a more desirable business model - moving from a volume-based revenue model to an all-you-can-carwash, subscription-based revenue. At this point, it seems like subscription as a business concept has been overused and overplayed - the term CWaaS (Car-wash-as-a-service), as some have tried to market this as, might be the last straw - but there are very real benefits to subscription for car washes, under the right conditions. Especially for automatic car washes, where marginal costs are low given most of the expenses are in upfront capital spend to build the car wash, subscription can be an attractive, high-margin way to grow given a well thought-through subscription strategy can make customers consumer more than they would otherwise. If it costs $10/car wash and customers on average wash their cars twice a month, and you charge $25 for unlimited monthly car washes, customers can do the quick math and realize that each incremental car wash under a subscription costs $5 or less - and who wouldn't want to pay up to have a permanently clean car? This locks in an immediate 25% revenue uplift, not to mention profit uplift in excess of 25% as you'll get more leverage on your fixed costs - not to mention an increased reliability to revenues as customer retention jumps. Together, these drive increased volumes and a more stable business model - making car washes a far more attractive opportunity than before.

Note that this all has to assume low marginal costs, and why this model has mainly worked for car washes that are automatic. If marginal costs are high, a subscription model could backfire as customers have a conflict of interest with the business - they are incentivized to consume as much as possible to reduce their average costs, and with each increased unit of consumption under a subscription, profit margins for the business decline, and could potentially go negative. That is why we don't see all-you-can-eat salad subscriptions - if we can pay a fixed dollar amount to get all the salad we want in the month, the only consumers who will sign up will be those who eat salads as much as possible - which boosts revenues, but will ultimately hurt profitability.

Taken together, the DIFM and subscription tailwinds have created the opportunity for car washes. This has been further accelerated by the financing side of the equation.

Sale/Leaseback Financing - The economics for car washes is further accelerated by an increased comfort on the part of real estate investors to invest in car wash real estate. Pre-financing, car washes are already quite profitable ventures with decent returns - on $6mm of initial capex (capital expenditure) spend, owners can get $1.2mm of profitability (EBITDA, or earnings before interest, taxes, depreciation and amortization, which is a decent proxy for cash flows) - per estimates from one of the largest car wash businesses Mister Car Wash. This is an 19% return on capital, which is decent:

Expected Run-Rate Profitability (Smm)

Returns on Initial Ca*x")

However, by accessing the financing markets for car wash real estate, owners of car washes can further enhance their returns by selling their real estate to external investors, and then leasing it back. Given increased investor comfort in car wash real estate, they're willing to do this for fairly low cost - 6.5% cap rates, i.e. car washes sell their real estate to investors, and in return, pay an annual lease rate that is 6.5% of the total value of the real estate. For an average $6mm car wash, this real estate is typically worth $4mm, which reduces the net capital spend to $2mm. This reduces profitability from the ~$1.2mm to ~$900k, as the car wash now pays $4mm x 6.5% = $260k in lease costs. Doing so more than doubles the return on investment, to 45%.

(-) Sale-leaseback Proceeds

Net Capex Spend

Run-Rate Profitability ($mm)

(-) Lease Costs

Run-Rate Profitability (Post Lease, $mm)

Returns on Initial

6.0

(4.0)

2.0

1.2

(0.3)

0.9

45.0%")

19% returns are very commendable to begin with, but 45% - that hits it out of the ballpark. If one starts out with $2mm, builds a car wash, then reinvests all the cash flows from our one car wash into building new car washes, one can very quickly build a car wash empire. The simple model below shoes how 1 car wash with a consistent 45% return on investment profile can and will grow into 27 car washes paying out ~$25mm per year by the end of 10 year.

(+) Car Washes Built

# Car Washes (End)

Profitability ($mm)

Cash Balance (Start)

(+) profitability

(-) Spend on New Car Wash)

Cash Balance (End)

Assumptions

profitability/Car Wash ($mm)

Cost/Car Wash ($mm)

0.9

0.9

0.9

$20

0.9

0.9

0.9

$20

0.9

1.8

0.9

(2.0)

$0.9

$2.0

1.8

1.8

(2.0)

$0.9

$2.0

(2.0)

1.2

$0.9

$2.0

3.6

3.6

(4.0)

0.8

$2.0

08

(6.0)

$20

(8.0)

$20

11.7

0.3

11.7

(12.0)

$0.9

$2.0

10

19

27

17.1

17.1

(16.0)

1.1

$0.9

$2.0")

A pretty incredible outcome. Of course, in reality there will be nuances to whether the 45% returns can be achieved across the entire portfolio of car washes given real execution risks to each new car wash being built (Is there enough traffic at the location? Are there competitors?), but if one becomes very adept and opening new car wash locations, the economics can be very compelling.

External Capital - Which brings us to the final driver of growth, the influx of capital looking to make these returns. Anyone looking at the numbers above has to be raising their hand and asking how to invest. Which has been the case across the car wash industry. Not only are existing owners awash (ha) in cash and capital from their existing car washes and looking to open more locations, but external private equity firms have also gotten involved - the Bloomberg article notes over 50 (!) different groups (and this likely doesn't include existing car wash owners) trying to buy and/or build new car washes.

This influx of capital is typically the final step in accelerating growth, for the floods of capital that enter an industry to take advantage of great economics will often dwarf any growth the industry can achieve on its own. And as long as demand exists, more car washes will certainly lead to more revenues for the industry - and it is this final financing driver that allowed car wash growth to take off in the past decade.

So ultimately, growth came about when opportunity - the latent demand for car washing from DIFM and the improved business model from subscription - met financing - the availability of cheap real estate investment capital and external capital influx into the car wash industry. Financing (real estate capital) drove opportunity, which led to incredible returns that lured in substantial amounts of external capital. The perfect environment for car wash growth, and the recipe for the rapid acceleration in car wash penetration in the US.

Awash in… Competition?

To me, the issue with the car wash business model is its replicability. There really is nothing that special about a car wash. While I'm sure there is a skill to picking the right location, building the car wash, and then attracting customers, it just isn't a defensible competitive advantage in the long term. No one really cares where they get their cars washed - so building a brand doesn't seem to add much value. The fifty financing groups that are looking to replicate the car wash unit economics via buying or building shows just that - anyone can build a car wash and access the great economics associated with it today. And if anyone can do it, and as capital floods into the space, we will hit a point where the industry becomes awash with so many car washes that the 45% return on capital economics that car washes get today will get competed away, as incremental car washes built start to cannibalize the customer bases of existing car washes, driving down revenues and profitability.

It's a trend we've seen time and time again - growth in a fragmented industry with limited barriers to entry, followed by oversaturation, followed by bankruptcies of some players, and eventually, consolidation and equilibrium. While often it's easy to think of growth in an industry as fairly steady:

In reality, there's far more happening under the surface, with various peaks and troughs along the way. Equilibrium in competitive markets typically isn't found overnight - rather, it's typically found after tumult, as the industry as a whole overbuilds and then has to go through the pain of rationalizing capacity before reaching equilibrium.

I expect the car wash industry to eventually go through the same process - where at some point, the industry overbuilds relative to the actual demand level, leading to oversaturation. This eats into unit economics for car washes as utilization falls, driving revenue and profitability lower. Given the low marginal cost of car washes (especially automatic ones), this likely ends up encouraging price wars as car washes attempt to maximize utilization, since marginal revenue dollars likely convert to profitability very well (each incremental car wash they give / subscription they sell is highly profitable as most costs are fixed). As prices fall, industry revenues fall, however given it takes time for new car wash growth to stall, the number of car washes will continue to grow. This further exacerbates profit and revenue issues for car washes, leading to substantial declines in car wash profitability (see purple line above). Eventually, car wash growth will stall out as the deteriorating unit economics slows growth rates, and eventually, car washes will start to close and go bankrupt. As this happens, the unit economics of car washes remaining open start to recover - as there are fewer car washes competing for the same amount of industry revenue dollars. Eventually, the industry will come to a new equilibrium - but not until much pain has been felt by industry players.

I've looked at many companies over my career, and many of them have fallen into this bucket - an undifferentiated player in an industry that is in the midst of explosive growth. Each time I've run into the same issue - even if I were to believe in the explosive growth ahead for the industry, how can I invest in this company, knowing that the industry and company will eventually hit oversaturation, and still be able to sleep well at night?

The easy answer has been to take the "better be safe than sorry" approach and avoid investing at all, using the eventual intensity of competition as an excuse to not invest. Not an entirely bad option, especially if your goal is to find 10-20 really good companies and hold them for the long-term. And one many investors would make given the importance many ascribe to long-term, durable, competitive advantages in their investment decisions and the quick rejection of companies that do not have these advantages.

But as I reflected on the car wash industry this week, I think there's another layer of analysis that we could and should do before any investment decision.

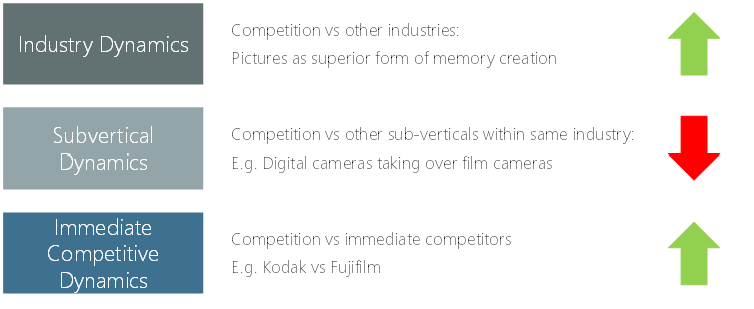

Ultimately, competition exists at many - even every - level of abstraction. A mistake I often make is placing too much weight on company level competition, and failing to think through the higher levels of competition.

If we took ourselves back 20-30 years to look at the film camera industry and think through the competitive dynamics then, it's fairly obvious that we have to think about competition across all levels - rather than myopically focus on the level we are most comfortable thinking about.

Say one were to come to the decision that Kodak were a great company with a strong brand name and technological advantages vs peers. This might have made for a compelling investment case.

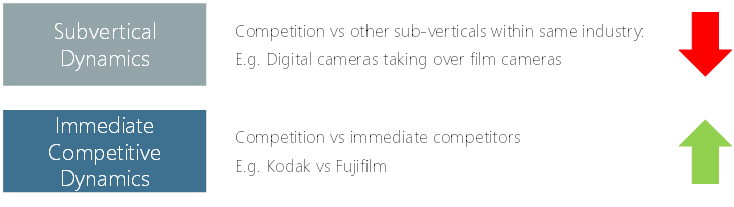

However, if one were to dig into the changing dynamics at the industry subvertical level, i.e. the competition taking place between the digital camera subvertical and the film camera subvertical, then a Kodak investment certainly no longer looks as compelling - certainly the case given the benefit of hindsight:

This would suggest that changing competitive dynamics at higher level of abstractions naturally trounce those at lower levels - no matter how good a business is relative to its immediate competition, if there are clear, powerful, competitive forces taking place at a higher level, they will outweigh any competitive benefits at a lower level.

That being said, not every higher level competitive dynamic will outweigh lower level competitive dynamics, for even if we considered the broader industry trend of cameras "taking share" from faulty human memory for the purpose of memory creation, which was a huge positive tailwind, this wasn't enough to salvage the investment case for Kodak. Digital cameras (at least for the time being until smartphones came around) took all the benefits that this higher-level, positive industry competitive dynamic conferred onto the industry.

Ultimately, my guess is that the subvertical dynamic was so powerful that it sucked the air out of the industry for the film camera industry, rendering any competitive dynamics at the film camera industry level irrelevant.

What this all means is the following. First, it's essential to have a broad understanding of all the competitive forces taking place that are relevant to a company, and not just myopically focus on certain levels. Second, all else equal, the higher the level of abstraction at which the dynamics are taking place, the more powerful and therefore, the more important they are. But third, it's crucial to have a good grasp of the magnitudes of the competitive forces at different levels, for weak, higher level competitive forces can be outweighed by stronger but lower level competitive forces.

Taking this back to the chart from above: while most of the time (equilibriums + periods of oversaturation), immediate competition is the most important factor, it's in periods of outsized industry growth, which tend to happen when a company's subverticals and/or industries are outcompeting and "winning" vs other groups, where the immediate competitive dynamic does not matter, for the higher level competitive forces trounce anything occurring at the immediate competitive level. This makes sense, as the growth provides each individual participant with more than enough, so there's no in-fighting going on. But once the pie stops growing as quickly, that’s when all players start fighting over the pie and things get ugly. Knowing the biggest and strongest at that point is what matters.

It is thus essential that companies and investors identify where their businesses sit on the curve above when deciding whether to invest in the face of poor immediate competitive dynamics. Catch a company that's within an industry early enough in its growth phase, and focusing too much on immediate competitive dynamics could end up causing a painful "no" investment decision.

-----

That's it for this week. Thanks for reading as always (especially if you made it all the way here)!